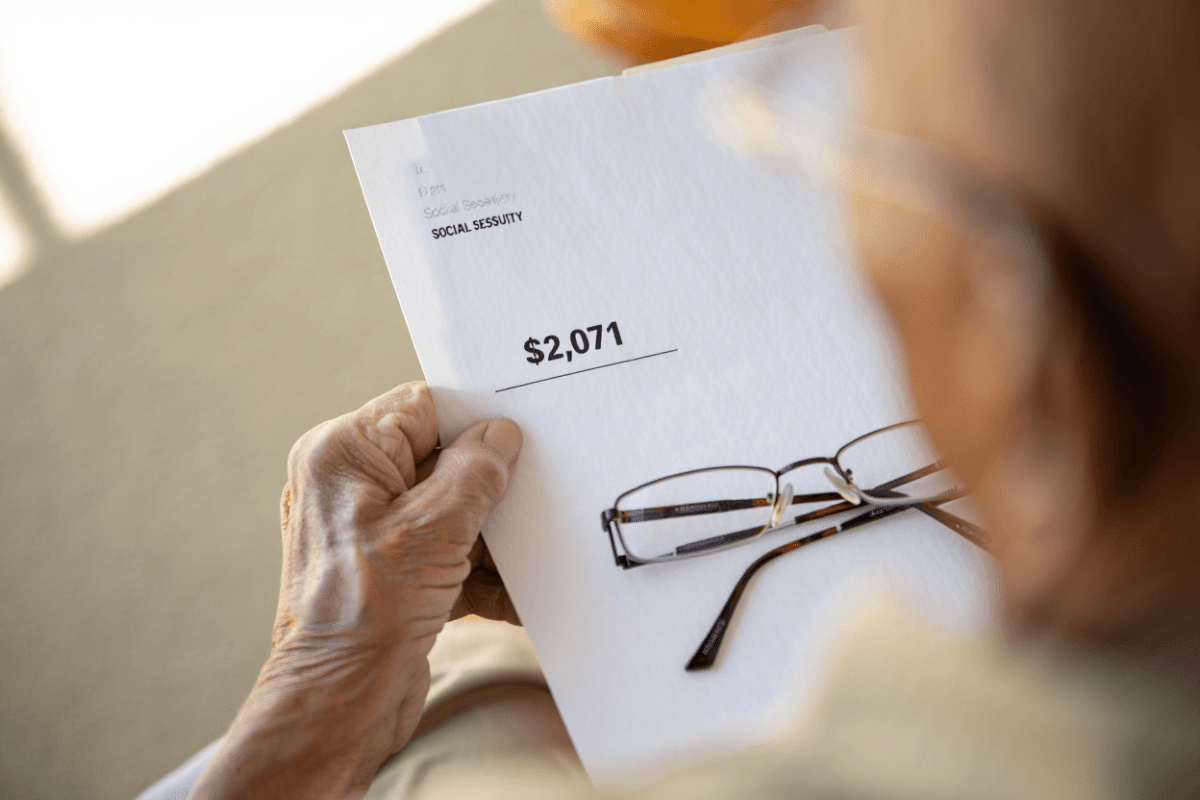

Nearly 71 million Social Security beneficiaries will receive a 2.8% increase in their monthly benefits starting in January 2026, according to the Social Security Administration. This cost-of-living adjustment (COLA) boosts the average monthly retirement check by approximately $56, from $2,015 to $2,071 for retired workers. The adjustment affects not only retirees but also disabled workers and survivors, representing one of the most consequential benefit changes in recent years.

🔥 Quick Facts

- 2.8% COLA increase applies to all 71 million beneficiaries in January 2026

- $56 monthly boost for average retired worker ($2,015 → $2,071)

- Married couples receiving joint benefits gain approximately $94 per month

- First increase above 2.5% since 2023, reflecting inflation recovery

- 7.5 million disabled workers and Supplemental Security Income recipients also benefit

Understanding the 2026 COLA: Why This Matters for Retirees

Cost-of-living adjustments have become increasingly significant for retirees facing persistent inflation. The 2.8% COLA for 2026 represents a meaningful recovery compared to the 2.5% adjustment in 2025, signaling that the Social Security Administration is responding to real inflationary pressures affecting seniors. For beneficiaries living on fixed incomes, even modest increases can meaningfully impact purchasing power and financial security.

The January 2026 implementation date ensures that checks reflecting the increase reach beneficiaries with their December benefit payments paid in early January. This timing allows seniors to plan expenses for the new year with confidence in their adjusted income level. The announcement came on October 24, 2025, giving beneficiaries advance notice to budget accordingly.

Breaking Down the Benefit Increases by Beneficiary Type

The 2.8% increase applies uniformly across all Social Security beneficiary categories, but the dollar amounts vary based on earning history. According to Social Security Administration estimates, the increases are distributed as follows:

Retired workers represent the largest group, averaging $56 monthly gain. However, those who delayed benefits beyond full retirement age receive substantially higher monthly amounts and thus larger absolute increases. For example, someone receiving $4,000 monthly would gain $112 under the same 2.8% formula.

2026 Benefit Amounts: A Comparative Table

The Social Security Administration released official estimates showing benefit levels before and after the 2.8% COLA adjustment. These figures provide critical context for understanding individual impact:

| Beneficiary Category | Before 2.8% COLA | After 2.8% COLA | Monthly Increase |

| All Retired Workers (Average) | $2,015 | $2,071 | +$56 |

| Aged Couple (Both Retired) | $3,234 | $3,328 | +$94 |

| Disabled Workers (Average) | $1,550 | $1,594 | +$44 |

| Maximum Individual Benefit (at FRA) | $4,035 | $4,152 | +$117 |

| SSI Federal Payment (Individual) | $967 | $994 | +$27 |

The increases ripple through the entire retirement income system. Beneficiaries who rely on Social Security as their primary income source will experience modest but meaningful relief from inflation pressures. Additionally, Social Security delivers historic improvements in service delivery support these benefit enhancements, creating a more comprehensive modernization of the program.

“The 2.8 percent cost-of-living adjustment will begin with benefits payable to nearly 71 million Social Security beneficiaries in January 2026. This increase reflects the continued commitment to ensuring that Social Security benefits keep pace with the cost of living.”

— Social Security Administration, Official COLA Announcement, October 2025

Policy Implications and Future Beneficiary Protections

This 2.8% increase demonstrates how COLA mechanisms work to protect seniors from inflation erosion. However, policymakers continue debating long-term Social Security solvency, including the trust fund depletion timeline projected for the 2030s. The 2026 increase comes as Social Security proposes rule changes affecting disabled workers, creating a complex landscape where benefit enhancements coexist with policy scrutiny.

Beyond the immediate 2.8% boost, beneficiaries should understand that future COLA adjustments depend on inflation measurements tracked through the Consumer Price Index. Higher inflation in late 2025 contributed to the 2.8% determination, while moderating inflation could result in smaller or larger adjustments for 2027. The program’s sustainability remains a central policy concern even as current beneficiaries receive tangible relief.

What Does a $56 Monthly Increase Mean in Practical Terms?

For the average retired worker receiving $2,071 monthly, the additional $56 translates to approximately $1.87 per day. While modest in isolation, this increase compounds over time and addresses real cost pressures. A retiree purchasing groceries, managing prescription medications, or paying utilities will recognize the cumulative benefit across essential categories. The increase arrives annually, meaning beneficiaries gain approximately $672 yearly before any 2027 adjustments.

The timing of benefit increases also matters. Beneficiaries receiving their enhanced payments throughout 2026 experience improved financial breathing room during months when healthcare costs peak and winter utility bills surge. For married couples receiving $3,328 monthly, the $94 increase provides nearly 3.5% additional discretionary income—often sufficient to cover increased food and energy costs without budget reductions elsewhere.

How Does the 2026 COLA Compare to Historical Trends?

Understanding the 2.8% increase requires context. The 2025 COLA was 2.5%, while 2024 saw a 3.2% adjustment. Earlier years saw dramatically different rates: the 2022 COLA increased 8.7% due to pandemic-related inflation, while 2021 saw only a 1.3% increase. The 2026 rate of 2.8% falls between recent historical patterns, suggesting a stabilizing inflation environment relative to 2022 peaks but continued cost pressures affecting retirees.

Experts track these variations because they signal whether Social Security recipients are maintaining purchasing power relative to the broader economy. A 2.8% increase below inflation rates would erode benefits over time, while increases above inflation would enhance purchasing power. Most economists indicate that 2026’s adjustment reasonably addresses inflationary pressures, though individual spending patterns vary by geography and lifestyle.

What Questions Should Beneficiaries Ask About Their 2026 Benefits?

As the January 2026 implementation date approaches, beneficiaries should verify their expected new monthly amount through their my Social Security account online or by contacting a local field office. Those receiving supplemental income, veterans benefits, or railroad retirement combined with Social Security should confirm how the 2.8% increase affects their overall benefit package. Additionally, beneficiaries approaching full retirement age should understand how the increased benefit amount impacts future earning limitations and spousal benefits.

Circumstances change, and the 2026 COLA announcement provides opportunity for beneficiaries to reassess retirement income plans, evaluate work opportunities, or adjust healthcare cost projections. Those concerned about long-term program sustainability may also use this moment to discuss Social Security planning with financial advisors to ensure comprehensive retirement security beyond government benefits alone.

Sources

- Social Security Administration – 2026 Cost-of-Living Adjustment Fact Sheet and Official COLA Announcement

- Social Security Administration Office of the Actuary – Benefit Payment Estimates and COLA Calculations

- AARP – Analysis of 2026 COLA Impact on Beneficiaries

- Kiplinger and Investopedia – Average Monthly Social Security Benefit Tracking