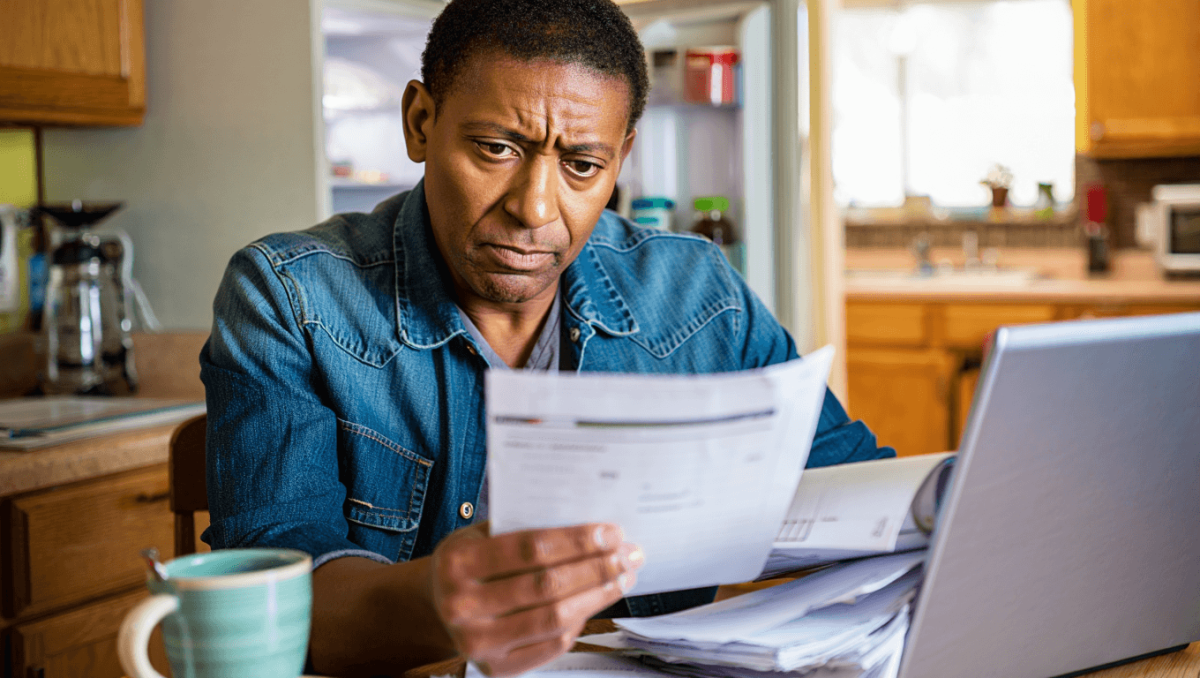

A recent PwC Employee Financial Wellness Survey finds members of Generation X increasingly delaying retirement as rising living costs and stagnant pay squeeze household budgets. The shift is no longer a distant concern: it is reshaping personal finances now and creating real planning headaches for employers.

The study reports that roughly half of Gen X workers are postponing their planned retirement dates. Just under four in ten believe they can still retire on schedule, and a majority say they may tap retirement savings early to meet short-term needs—moves that can reduce retirement income and complicate future financial stability.

| Measure | Share of respondents |

|---|---|

| Gen X delaying retirement | ~50% |

| Believe they can retire as planned | 38% |

| Expect to withdraw from retirement accounts early | More than 50% |

| Workforce with no short-term financial buffer | 25% |

| Workers saying pay isn’t keeping up with costs | 49% |

| Employees who feel unequipped to handle a financial crisis | 41% |

PwC’s analysis points to one central driver: employees’ inability to build or maintain liquid savings as everyday expenses outpace income gains. The survey finds many households are making recurring trade-offs just to cover essentials, leaving little room to save for retirement or weather an emergency.

The practical consequences are layered. For individuals, early withdrawals and delayed retirement translate into smaller nest eggs and potential tax or penalty costs; for companies, the trend can stall promotion pipelines and raise benefits and payroll expenses as older workers remain on the job longer than planned.

- Workforce planning: Delayed exits create gaps in succession timing and talent development.

- Cost pressures: Extended tenure of higher-paid employees can increase labor and benefit expenses.

- Employee engagement: Financial stress during peak career years may reduce focus and productivity.

What employers — and employees — can do now

PwC urges companies to treat financial wellness as an active workplace issue rather than a peripheral benefit. The report recommends normalizing financial education, offering human-led coaching, and shifting some support toward daily money management skills that help employees handle immediate pressures.

For employers, that means embedding practical resources into the employee experience: approachable coaching, clearer communications about plan options, and training that builds confidence around routine financial choices. For workers, the priority is improving liquidity where possible—small emergency cushions, budgeting support, and using employer-provided planning tools before resorting to retirement withdrawals.

Survey respondents described the barriers as less about unwillingness and more about feeling unprepared: many want financial stability but lack the tools to get there. That gap—between desire and capability—is where both policy and workplace benefits can make a measurable difference.

The ripple effects are immediate. If large cohorts of experienced employees continue to postpone retirement, companies will face tougher decisions on hiring, compensation structures and long-term succession. For households, delayed retirement and early account withdrawals raise the risk that years of work will not translate into secure retirement income.

Addressing this problem will require coordinated action: clearer employer programs, better access to financial coaching, and policies that help workers build short-term buffers. Without those steps, the trend of stretched careers and strained household finances is likely to persist, with consequences felt in offices and living rooms alike.