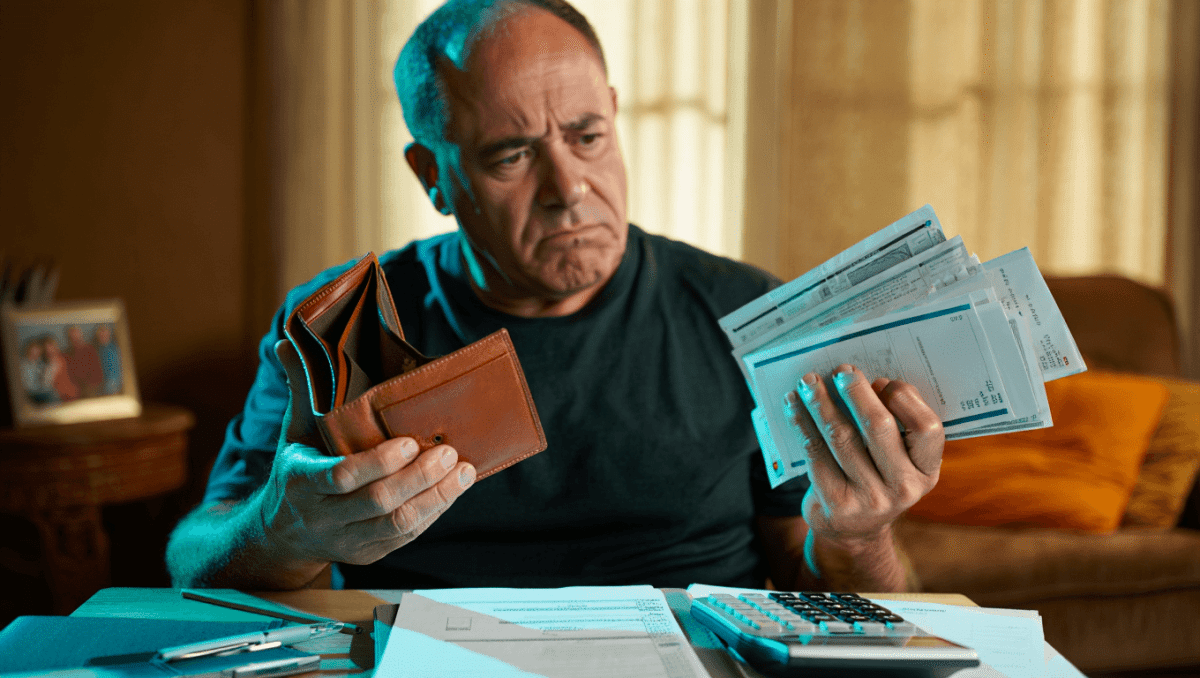

Gen X faces a retirement reckoning as nearly 50% can’t retire on schedule due to inflation, stagnant wages, and weak savings. A new PwC survey reveals the shocking financial squeeze hitting America’s “sandwich generation” in May 2026. Only 38% believe they can retire when originally planned, marking the worst performance of any generation.

🔥 Quick Facts

- Nearly 50% of Gen X pushing back retirement dates due to rising costs and stagnant wages

- Median Gen X retirement savings stuck at just $40,000, far below the $1.1 million needed

- $404,976 shortfall between expected savings and comfortable retirement needs per Schroders

- Inflation impact forces Gen X to make difficult daily trade-offs between bills and future security

The Inflation Crisis Crushing Gen X Retirement Dreams

Rising living costs are eroding savings faster than ever before. Gen Xers report that 49% say their compensation isn’t keeping pace with expenses according to PwC’s latest Employee Financial Wellness Survey released April 29, 2026. This generation, now in their 40s and 50s, face a perfect financial storm. Household expenses surge while paycheck growth stagnates, leaving no room to boost retirement contributions.

The math is brutal. An annual $50,000 retirement expense could balloon to $102,000 in 25 years at historical inflation rates. Without aggressive action now, Gen X risks working well into their 60s just to meet basic retirement needs. More than half admit they cannot meet basic household expenses, let alone save meaningfully for the future.

Why Gen X Started Too Late and Can’t Catch Up

This generation faces a unique historical disadvantage. Gen X didn’t prioritize retirement savings until age 50 or later, according to Nationwide research from December 2025. They entered the workforce as traditional pensions vanished and 401(k)s arrived without auto-enrollment features. Many started contributing to retirement accounts at age 32 on average, leaving less time for compound growth compared to younger workers with automatic enrollment benefits.

The shift from pensions to 401(k)s created a generational disadvantage. Baby Boomers had guaranteed lifetime income, but Gen X shoulders individual investment risk. Without proper financial tools or education, many fell behind. The earliest Gen Xers are now turning 60 in 2026, and they’re realizing the gap may be too wide to close. With only 16% feeling adequately prepared for retirement, anxiety is at an all-time high.

The Sandwich Generation’s Hidden Burden: Student Loans and Caregiving

| Financial Pressure | Gen X Impact |

| Student Loan Debt | Average of $38,000 per Gen Xer with outstanding loans |

| Caregiving Costs | Supporting aging parents while covering kids’ college tuition |

| Household Budget Impact | Nearly half living without financial buffer for emergencies |

| Debt-to-Retirement Ratio | Most indebted generation in America, direct retirement threat |

Gen X carries the heaviest debt burden of any generation. Fortune’s May 17 analysis reveals this “sandwich generation” juggles aging parent care, adult children’s education costs, mortgages, and credit cards simultaneously. When debt payments take priority, retirement contributions stop. Gen Xers with outstanding student loans carry $38,000+ on average, considerably more than younger generations since they graduated decades ago but never paid them off.

Employers are starting to respond. Companies like Abbott now match 401(k) contributions while employees tackle student loans. The SECURE 2.0 Act enables this strategy, and nearly two-thirds of employers now offer debt assistance programs. However, this help arrives too late for millions already in financial distress.

The Widening Generational Savings Gap and What It Means

Gen X isn’t just behind on savings; they’re falling further behind daily. While 54% of non-retirees doubt they’ll be financially prepared, Gen X faces particular urgency. The oldest members are entering critical final working years when savings should accelerate, but inflation prevents it. Those over 55 show 28% are extremely or very concerned about insufficient lifetime income, twice the worry level of Baby Boomers at the same life stage.

Early withdrawals signal desperation. More than half of Gen Xers expect to raid retirement accounts early to cover short-term costs, a decision that snowballs into smaller nest eggs. Each decade of delay roughly halves retirement funds available. Gen X cannot afford to wait, yet inflation forces them to do exactly that. Some face the grim reality of 42% planning to return to work after retiring, according to Global Atlantic research, compared to just 21% of Boomers.

Can Gen X Still Save Their Retirement Before It’s Too Late?

The clock is ticking, but strategic moves exist. For Gen X still working, contributing the maximum $24,500 to a 401(k) in 2026, plus $7,500 in catch-up contributions if age 50+, provides a final push. Delaying Social Security from age 62 to 70 increases monthly benefits by 8% annually, potentially worth $100,000+ more over retirement. Even working 2-3 extra years provides compound growth opportunities that seem impossible today.

The hard truth: Most Gen Xers won’t retire as planned. Some will work longer voluntarily, others by necessity. Financial advisors urge addressing student loans aggressively, cutting discretionary spending now, and exploring alternative income streams. Yet without wage growth matching inflation, individual effort hits a ceiling. Policy solutions may matter more than personal discipline at this point. Should Gen X demand employer involvement, stronger Social Security guarantees, or pension restoration?

Sources

- Fox Business – Nearly 50% of Gen X workers delaying retirement due to rising costs and stagnant wages, PwC survey findings from April 29, 2026

- Fortune – Gen X as the most indebted generation in America with highest student loan balances and employer support programs like SECURE 2.0, May 17, 2026

- Investopedia – Gen X expects $400K+ retirement shortfall due to 401k shift away from pensions, Schroders wealth management research findings