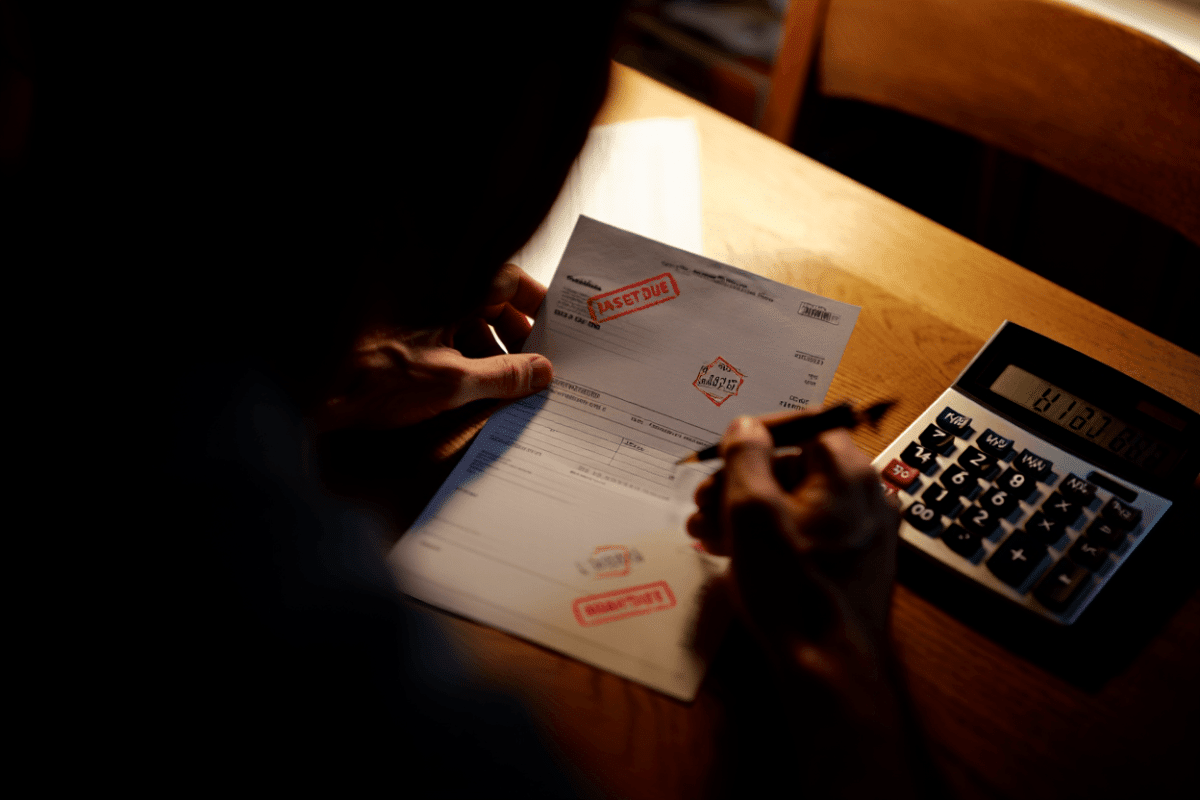

Credit card delinquencies in the United States have reached their highest level in 15 years, with 13.12 percent of credit card balances at least 90 days past due in the first quarter of 2026, according to the Federal Reserve Bank of New York. This marks the worst delinquency rate since the aftermath of the 2008 financial crisis.

The grim milestone comes as Americans carry a total of $1.25 trillion in credit card debt. The balances represent a significant increase from the previous quarter, when credit card debt stood at $1.18 trillion, marking a rise of $70 billion in just three months.

Soaring interest rates and stubborn inflation have been the primary drivers of the surge in delinquencies. As the Federal Reserve raised rates to combat inflation over recent years, credit card interest rates climbed alongside them, with the average APR reaching approximately 21 percent across all cards. The combination of higher borrowing costs and elevated prices for everyday goods has strained household finances, pushing more Americans to miss payments.

The current delinquency rate reflects a pattern analysts describe as “survival debt,” where consumers rely on credit cards to cover basic expenses like groceries and utilities rather than discretionary purchases. This shift signals that financial stress is no longer concentrated among subprime borrowers but has spread across income levels and age groups.

When credit card delinquencies reached peak levels during the 2008 financial crisis and its immediate aftermath, the economy faced a broader collapse in housing, employment, and consumer spending. Today’s delinquency rates, while approaching those crisis-era levels, occur in a different economic context—one shaped by inflation and elevated rates rather than a systemic banking failure. However, the sustained elevation of delinquencies suggests households are continuing to face pressure from the lingering effects of price increases and higher borrowing costs.

Sources

- Federal Reserve Bank of New York — Household Debt and Credit Report; confirmed $1.25 trillion in credit card balances and delinquency data for Q1 2026.

- Wall Street Journal — Reported that soaring interest rates and stubborn inflation have led to highest delinquencies since the financial crisis, with quote about “pattern of survival debt.”

- USA Today — Confirmed that roughly 13 percent of the nation’s credit card balance was at least 90 days delinquent in Q1 2026.

- CardRates.com — Confirmed 13.12 percent delinquency rate is the highest level in 15 years, with previous high during 2008 financial crisis aftermath.

- KTLA — Reported average interest rates running at about 21 percent on credit cards.