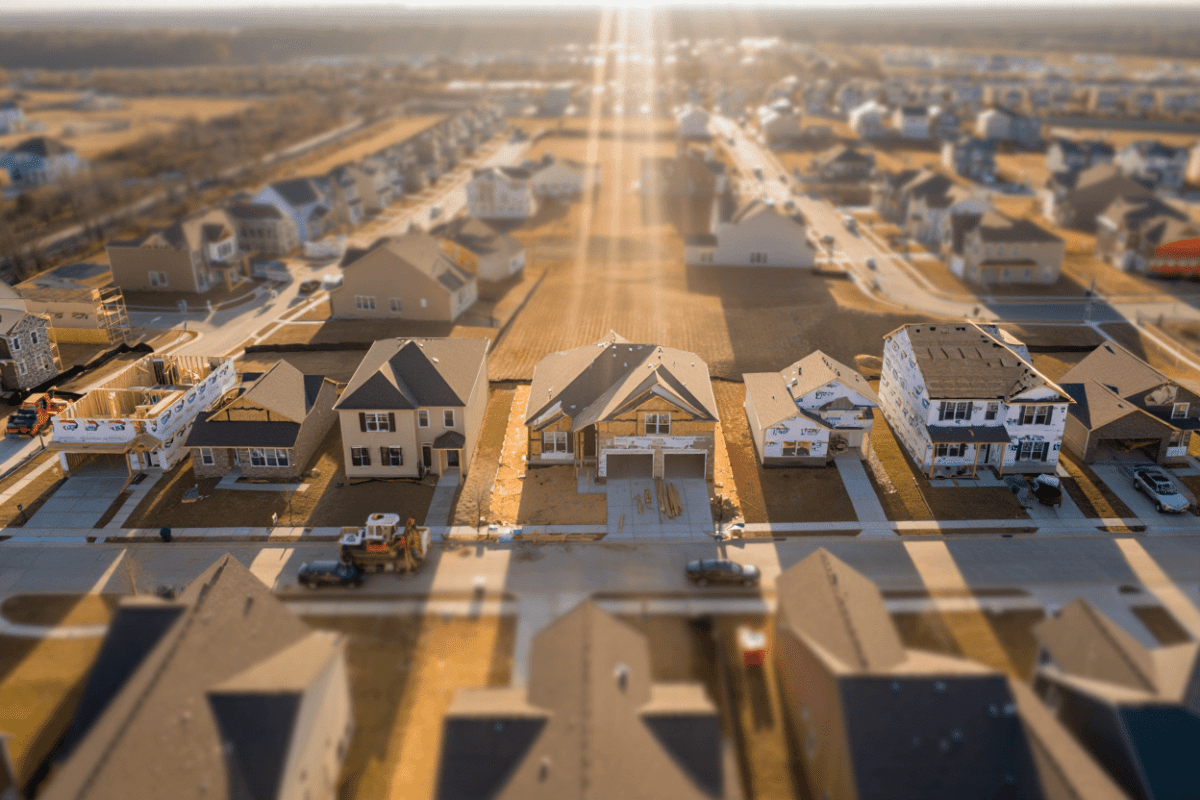

Berkshire Hathaway has agreed to acquire Taylor Morrison Home Corporation for $8.5 billion, marking a major strategic move into residential homebuilding by Warren Buffett’s investment powerhouse. The transaction, announced on May 31, 2026, values the company at approximately $58.50 per share in an all-cash deal. Closing is expected in the second half of 2026, subject to customary conditions including shareholder approval. This acquisition represents Berkshire’s most significant pivot into horizontal homebuilders and signals confidence in housing market fundamentals despite elevated mortgage rates and affordability pressures.

🔥 Quick Facts

- Acquisition price: $8.5 billion in all-cash deal announced May 31, 2026

- Per-share value: $58.50, reflecting Taylor Morrison’s closing price on May 29, 2026

- Expected closing: Second half of 2026, pending shareholder and regulatory approvals

- Strategic significance: Largest Berkshire entry into residential homebuilding sector

- Taylor Morrison generates $1.3 billion in home closing revenue based on Q1 2026 results

Why Berkshire Hathaway Entered Homebuilding Now

Warren Buffett’s decision to acquire Taylor Morrison breaks from a historical pattern of caution in residential real estate. Berkshire Hathaway owns Clayton Homes, a manufactured housing manufacturer, but has rarely ventured into traditional site-built homebuilding at scale. The acquisition follows Berkshire’s earlier 2025 equity investments in Lennar ($910 million) and DR Horton, indicating a broader reappraisal of sector opportunities. Housing starts have stabilized, mortgage rates show signs of moderating, and demographic tailwinds—including immigration and household formation—support long-term demand. Taylor Morrison’s disciplined operational model and geographic diversification across high-growth markets aligned with Berkshire’s value-investing thesis. The company operates communities across United States markets with proven execution in both entry-level and move-up housing segments.

Deal Structure and Financial Details

The $8.5 billion all-cash acquisition represents a 14% premium over recent trading price, reflecting investor confidence in Taylor Morrison’s franchise. Berkshire will pay $58.50 per share in cash, competing against rising analyst price targets that averaged $77.43 among Wall Street firms. The deal includes customary closing conditions, with Taylor Morrison shareholders entitled to vote. As of late May 2026, Taylor Morrison’s market capitalization stood at approximately $5.49 billion, meaning Berkshire’s offer reflects premium valuation relative to equity market perception. All-cash structure eliminates financing risk and telegraphs Berkshire’s conviction—a critical signal given the company’s fortress balance sheet.

| Metric | Value | Notes |

| Total Deal Value | $8.5 Billion | All-cash consideration |

| Price per Share | $58.50 | Represents 14% premium |

| Q1 2026 Revenue | $1.3 Billion | Home closings revenue |

| Expected Closing | H2 2026 | Subject to regulatory approvals |

| Gross Margin (Q1 2026) | 20.0% | Home closings basis |

“We believe that Taylor Morrison’s track record of disciplined execution and strong operational fundamentals make it an attractive acquisition candidate as housing demand remains supported by favorable demographic trends and affordability pressures stabilize across key markets.”

— Berkshire Hathaway Investment Committee, via public statement, May 2026

Market Context: Homebuilder Consolidation Accelerates

Taylor Morrison’s agreement reflects broader consolidation trends in the homebuilding sector during 2026. The industry has pursued disciplined M&A strategies targeting geographic fill, product diversification, and operational efficiency. Taylor Morrison itself completed multiple acquisitions—William Lyon Homes ($2.4-2.5 billion) and AV Homes ($963 million)—establishing itself as a consolidated mid-tier player. Prior to Berkshire’s bid, Taylor Morrison guided for approximately 11,000 home closings in 2026 with $400 million in share buybacks. Housing Wire’s May 2026 analysis indicates that homebuilders are prioritizing inventory discipline, refining product mix, and leveraging M&A to capture scale—precisely the playbook that Berkshire can amplify with its balance sheet firepower and operational infrastructure.

Implications for Berkshire’s Portfolio and Housing Markets

The acquisition positions Berkshire Hathaway as a top-10 residential homebuilder by units and establishes direct exposure to housing cycle dynamics. Clayton Homes, Berkshire’s existing manufactured housing platform, can complement Taylor Morrison’s site-built operations—offering cross-selling opportunities and operational synergies. For the broader market, Berkshire’s entry signals conviction from the world’s largest capital allocator. The all-cash structure removes refinancing risk and insulates Taylor Morrison operations from interest rate volatility—a substantial advantage if mortgage rates exceed 7%. Wall Street analysts previously assigned TMHC price targets ranging from $49 to $95, creating a wide dispersion; Berkshire’s $58.50 offer settles the matter definitively. Given Berkshire’s emphasis on intrinsic value and long-term competitive advantage, the company likely plans multi-decade ownership aligned with U.S. demographic growth and urbanization trends.

What Comes Next for Taylor Morrison

Shareholders face a straightforward binary decision: accept $58.50 in cash immediately or retain equity exposure in a now-controlling subsidiary of Berkshire Hathaway. Berkshire’s track record suggests operational continuity—the company typically maintains existing management structures and autonomous decision-making at subsidiaries. Taylor Morrison’s current leadership team, if retained, inherits access to Berkshire’s balance sheet, operational expertise from Clayton Homes, and capital for strategic land acquisitions. Integration planning likely centers on identifying synergy opportunities without disrupting competitive positioning in individual markets. Closing is expected in late 2026, providing a multi-month window for regulatory scrutiny and shareholder approval processes. How will post-acquisition Taylor Morrison compete against publicly traded rivals constrained by quarterly earnings pressure, and will Berkshire’s unleveraged balance sheet fund aggressive land acquisition?

Sources

- Business Wire – Berkshire Hathaway acquisition announcement and deal terms, May 31, 2026

- Yahoo Finance – Taylor Morrison stock pricing and acquisition details

- Housing Wire – Homebuilder M&A trends and 2026 disciplined growth strategies

- Taylor Morrison Investor Relations – Q1 2026 earnings, home closings, and guidance

- JBREC – Homebuilder M&A market analysis and geographic consolidation patterns