Vertiv Holdings (NYSE: VRT) announced the acquisition of Strategic Thermal Labs on April 27, 2026, a strategic move cementing its dominance in liquid-cooling infrastructure for AI data centers. The deal bolsters Vertiv’s thermal management portfolio at a critical inflection point when AI infrastructure demand is reshaping the energy and cooling sectors. With backlog exceeding $15 billion and recent earnings showing 83% adjusted EPS growth, VRT stock has emerged as the pure-play thermal solutions provider for the AI boom.

🔥 Quick Facts

- Vertiv acquired Strategic Thermal Labs on April 27, 2026, adding cold-plate design and server-side liquid-cooling capabilities.

- VRT stock up 86% since January 2026, outperforming broad market indices on AI infrastructure momentum.

- Q1 2026 order backlog reached $15 billion, representing more than double year-over-year growth and visibility through 2027.

- First-quarter net sales rose 30% to $2,650 million as companies rush to deploy AI cooling infrastructure.

Why Liquid Cooling Defines the AI Data Center Arms Race

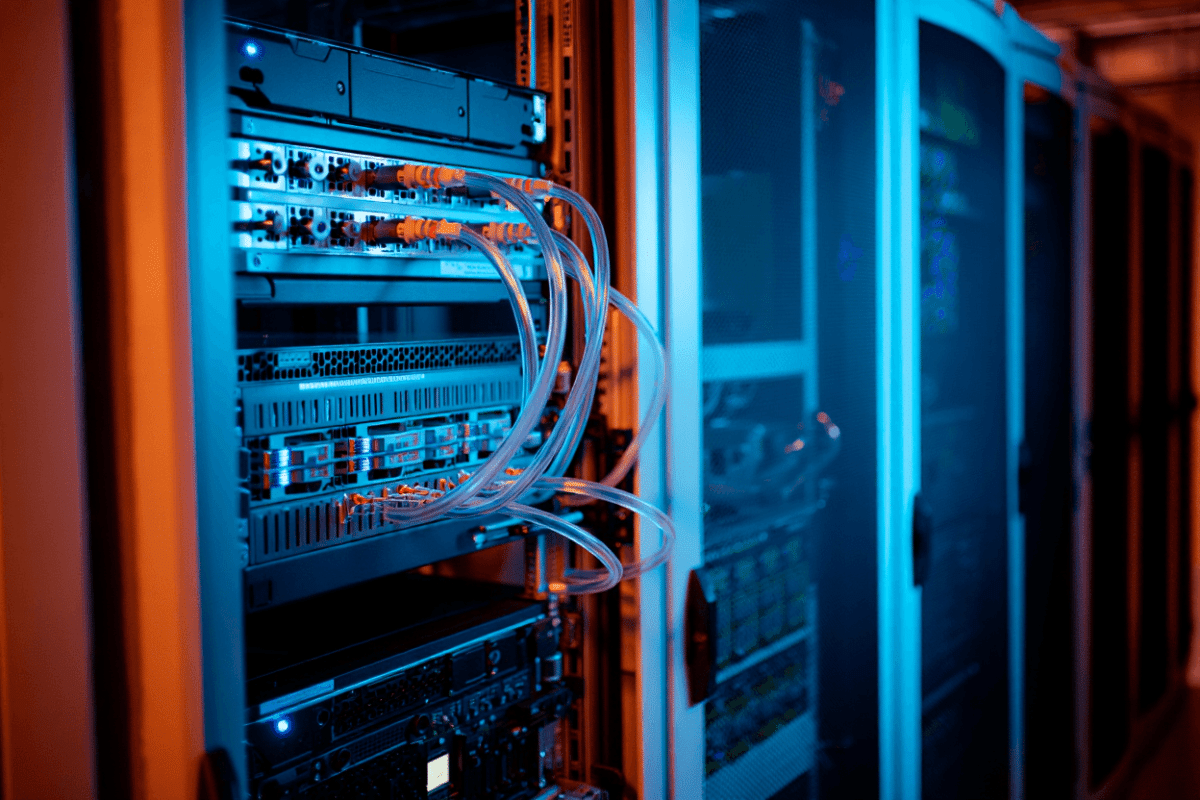

AI accelerators generate extreme heat—modern GPUs consuming 400-600 watts each in high-density configurations. Server farms deploying thousands of processors create thermal challenges that traditional air-cooling cannot resolve. Liquid-cooling systems remove heat 10 times more efficiently than air-cooled alternatives, allowing operators to pack more computational density into smaller physical footprints.

Vertiv’s Strategic Thermal Labs acquisition strengthens its ability to engineer solutions at the critical interface between servers and liquid infrastructure. The cold-plate technology developed by STL enables direct immersion cooling—a methodology gaining traction among hyperscalers like Meta, Google, and Amazon. This acquisition extends Vertiv’s thermal-chain strategy from facility-level cooling to component-level thermal management.

Strategic Positioning in a $100 Billion MarketOpportunity

The global data center cooling market exceeded $45 billion in 2025 and projects compound annual growth of 18% through 2030. Liquid-cooling represents the fastest-growing segment, driven by AI chip adoption and energy efficiency mandates. Vertiv’s market position rivals established competitors like Trane Technologies, Eaton, and Carrier, but with sharper focus on the AI infrastructure niche.

The acquisition demonstrates Vertiv’s disciplined M&A strategy, following earlier deals including ThermoKey (announced March 2026) for heat-rejection technology. As detailed in recent analysis of AI infrastructure investments, companies positioning for AI deployment are prioritizing specialized vendors. Vertiv’s acquisition cadence places it ahead of contract-focused competitors in building integrated capabilities.

Financial Momentum and Execution Risk

The numbers underlying VRT’s recent surge merit scrutiny. Q1 2026 diluted EPS grew 136% (to $1.03 per share) while adjusted EPS climbed 83% (to $1.78 per share). Revenue growth of 30% year-over-year substantially outpaced typical industrial equipment companies. Backlog visibility through Q1 2027 provides rare clarity in capital equipment markets.

However, execution risk remains material. Converting a $15 billion backlog into revenue requires supply chain resilience and manufacturing capacity scaling. Semiconductor lead times for components supporting thermal systems remain extended. Vertiv must simultaneously integrate Strategic Thermal Labs while ramping production—a dual challenge that challenges even well-managed acquirers.

| Metric | Q1 2026 | Q1 2025 | % Change |

| Net Sales | $2,650M | $2,036M | +30% |

| Diluted EPS | $1.03 | $0.43 | +136% |

| Adj. Diluted EPS | $1.78 | $0.97 | +83% |

| Backlog | $15.0B | $6.8B | +120% |

| 2026 Full-Year Guidance | Raised to $10.6B+ organic sales growth; 28% projected | ||

Wall Street analyst consensus remains constructive, with 47% strong buy ratings against minimal sell recommendations. The median price target of $360 implies 14% upside from recent trading levels. Yet valuation concerns persist—VRT trades at 18x forward EPS, a premium justified only if AI infrastructure demand sustains the current trajectory.

“The acquisition of Strategic Thermal Labs strengthens engineering capability at the interface between server-side liquid cooling and facility-level thermal solutions, allowing Vertiv to deliver more differentiated, integrated offerings to hyperscale customers.”

— Vertiv Company Statement, April 2026 Press Release

Broader AI Infrastructure Ecosystem Implications

The Strategic Thermal Labs deal reveals how AI infrastructure consolidation is reshaping supply chains. Companies like those focused on nuclear power for AI must partner with cooling vendors to create complete solutions. Vertiv’s integrated approach—combining power delivery, thermal management, and infrastructure orchestration—positions it uniquely against fragmented competitors.

However, competitive pressure intensifies. Schneider Electric competition remains formidable in facility-level cooling. Datacenters built by cloud giants may develop in-house thermal solutions, reducing dependence on third-party vendors. Vertiv’s execution on organic innovation must complement its acquisition strategy.

What Success Looks Like in 2026-2027

Three critical milestones will determine whether VRT stock sustains its gains. First, backlog-to-revenue conversion—translating the $15 billion pipeline into actual sales requires flawless supply chain execution. Second, Strategic Thermal Labs integration—achieving operational synergies and avoiding integration delays. Third, margin resilience—maintaining adjusted EBITDA margins while scaling manufacturing and absorbing acquisition costs.

If Vertiv delivers 28% organic growth as guided while maintaining double-digit margin expansion, the stock could sustainably approach $400+. If backlog conversion disappoints or integration falters, multiple compression risks a $250-280 retest. Earnings execution through late 2026 will prove decisive.

Will Thermal Innovation Remain a Vertiv Monopoly?

Competitive responses loom. Parker Hannifin, Eaton, and Carrier each possess thermal technology capabilities and could pursue similar bolt-on acquisitions. Specialized startups in immersion cooling (e.g., CoolIT Systems, Liquid Galaxy) attract venture capital. Hyperscalers themselves may internalize cooling R&D.

Vertiv’s first-mover advantage in integrating thermal solutions for AI remains robust but temporary. By 2028-2029, thermal cooling may commoditize as multiple vendors achieve scale. VRT’s durability depends on sustained technological differentiation and customer lock-in through integrated platforms.

Sources

- Vertiv Investor Relations — Acquisition announcement and Q1 2026 earnings release, April-May 2026

- Yahoo Finance — Real-time stock data and analyst consensus ratings

- MacroTrends — Historical stock price data and 52-week highs

- Data Center Dynamics — Liquid cooling market analysis and competitor positioning

- Forbes, Seeking Alpha, and Simply Wall Street — Independent equity research and acquisition analysis