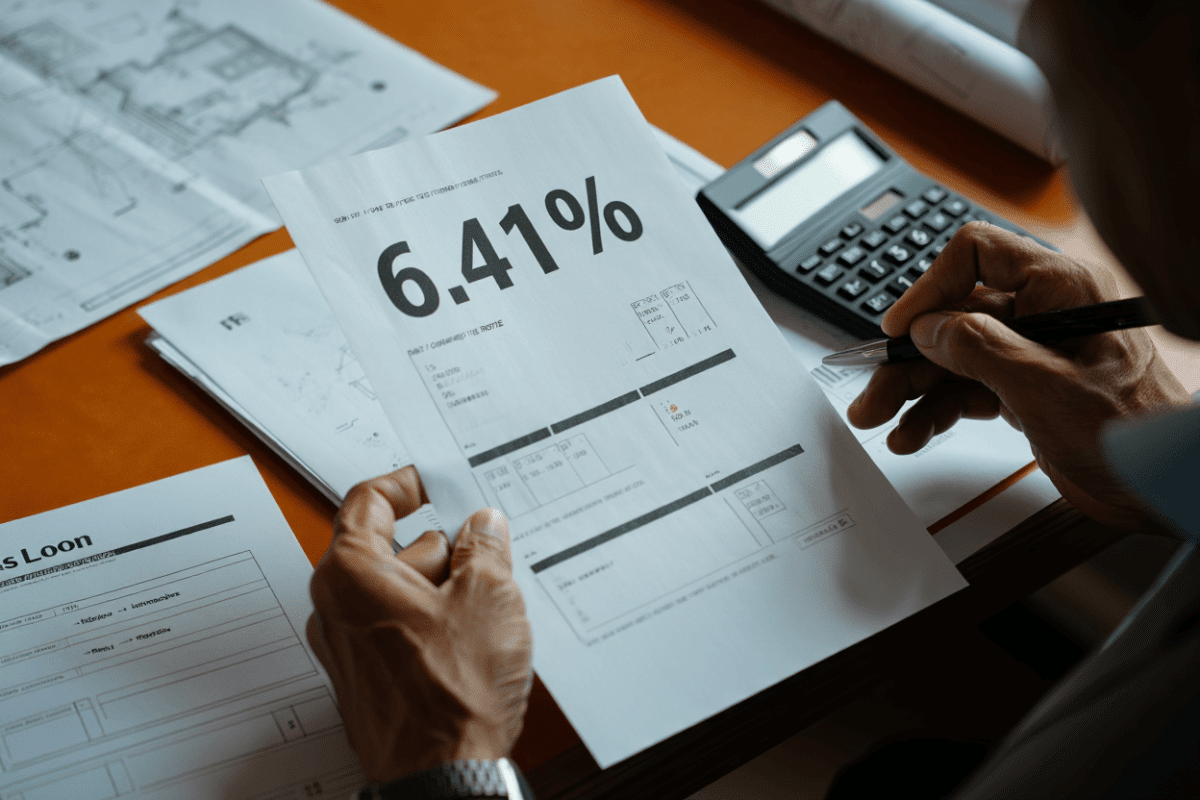

Mortgage rates hit 6.41% on May 23, 2026, marking a significant climb as the 30-year fixed-rate mortgage reached its highest level in 9 months. The surge reflects broader economic pressures, including persistent inflation concerns and the Federal Reserve’s decision to maintain interest rates at 3.50%-3.75%. This upward trajectory directly impacts housing affordability across the United States, forcing potential homebuyers to reassess their financial strategies in an increasingly expensive market.

🔥 Quick Facts

- 30-year fixed rate: 6.41% as of May 23, 2026

- Peak rate reached: 6.51% on May 21, 2026 — highest since August 2025

- 15-year fixed rate: 5.85%, up from 5.74% last week

- Federal funds rate unchanged: 3.50%-3.75% through May 2026

- Year-to-date rate change: Rates increased 0.23% from January 2026 average of 6.18%

Why Mortgage Rates Continue to Climb

The recent spike in mortgage rates stems directly from inflation concerns restraining the Federal Reserve from cutting rates as previously anticipated. When the year began, Wall Street expected multiple Fed rate cuts throughout 2026, but persistent inflation data—including core CPI readings remaining above the Fed’s target—forced policymakers to maintain a holding pattern. This creates a cascade effect through the mortgage market.

Mortgage-backed securities, which determine home loan rates independent of Federal Reserve policy, respond to Treasury yields and inflation expectations. As bond markets repriced in May 2026, anticipating that interest rates would remain elevated longer than previously forecast, mortgage rates climbed in tandem. The week ending May 21 saw the biggest surge, pushing the 30-year fixed rate to 6.51%—the highest point since August 2025, establishing a 9-month high.

Recent Rate Movement and Market Dynamics

Over the past week alone, rates have fluctuated significantly, revealing market sensitivity to economic data releases. On May 18, the rate stood at 6.41%, before climbing to 6.51% by May 21, then moderating slightly back to 6.41% by May 23. This volatility signals investor uncertainty about future Fed decisions and inflation trajectory.

The broader context matters: rates have climbed 15 basis points in just one week, suggesting accelerating upward pressure. According to Freddie Mac’s Primary Mortgage Market Survey, this represents the most significant weekly move in recent months. Some analysts attribute the volatility to recent inflation data triggering investor concern about persistent price pressures, which could force the Fed to maintain restrictive policy longer.

Rate Comparison and Historical Context

Understanding today’s rates requires historical perspective. Though 6.41% seems elevated, it remains significantly lower than the 7.08% peak reached in October 2023. However, compared to early 2026, when rates averaged 6.18%, the current environment represents a notable deterioration in affordability.

| Mortgage Type | May 23, 2026 | One Week Ago | One Month Ago |

| 30-Year Fixed | 6.41% | 6.26% | 6.30% |

| 15-Year Fixed | 5.85% | 5.74% | 5.79% |

| 20-Year Fixed | 6.39% | 6.25% | 6.28% |

| 30-Yr Purchase | 6.60% | 6.38% | 6.45% |

| 30-Yr Refinance | 6.96% | 6.67% | 6.82% |

The data reveals a consistent uptrend across all mortgage types. Even the lowest-cost 15-year fixed at 5.85% has risen 11 basis points in one week, indicating systemic rate pressure throughout the mortgage market. Purchase loans command a 19 basis point premium over refinance loans, reflecting lender risk assessment in a tightening market.

“Mortgage rates have been steadily climbing since April as markets reassess expectations for Federal Reserve policy. The recent jump to 9-month highs reflects investor concerns that inflation may persist longer than consensus forecasts suggested.”

— Mortgage Industry Analyst, Financial Services Research

Affordability Impact on the U.S. Housing Market

Mortgage rates at 6.41% translate directly into higher monthly payments for homebuyers. On a $300,000 home with a 20% down payment ($60,000), a borrower would pay approximately $1,432 monthly on a 30-year fixed mortgage—$35 more than just one week prior. This compounds the affordability crisis: rising rates have already pressured consumer debt levels across the economy.

Industry forecasters diverge on whether rates will fall or continue climbing. JPMorgan expects home prices to stall at 0% growth in 2026, while home sales gradually improve. Morgan Stanley predicts mortgage rates could decline to 5.75% by year-end, contingent on Fed rate cuts materializing. Fannie Mae, conversely, projects rates staying near 6.2% through 2026, suggesting current levels may persist or trend higher.

What Happens Next: Rate Forecast and Implications

The Federal Reserve holds its next regularly scheduled meeting in late June 2026. Current futures markets indicate virtually no probability of a rate cut at that meeting, with market expectations now pointing toward late 2026 at the earliest for any policy easing. This timeline suggests mortgage rates could remain elevated through summer and into fall, barring unexpected deflationary shocks.

Key economic indicators to watch include the June employment report, Personal Consumption Expenditures (PCE) inflation data, and consumer sentiment surveys. A cooling labor market could accelerate Fed rate cut signals, while stronger wage growth or continued inflation could force rates even higher. The sensitivity of 30-year mortgage rates to Treasury yields means that each Fed communication directly influences housing affordability decisions for millions of Americans.

Should Homebuyers Lock in Rates Now or Wait?

Financial experts remain split on rate timing strategy. Some argue that 6.41% represents a reasonable entry point compared to the 7%+ environment of 2023, making it prudent to lock in rates before they climb higher. Others recommend waiting until summer months, historically a period of mortgage rate volatility when broader market sentiment shifts due to geopolitical developments or economic data surprises.

Variables influencing this decision include credit score (borrowers with scores above 750 may qualify for rates 0.25-0.50% lower), cash reserves, loan-to-value ratio, and market conviction about future rate direction. As mortgage rates approach the 9-month high, the window for favorable refinancing opportunities appears to be closing, at least temporarily.

Sources

- Freddie Mac Primary Mortgage Market Survey — Weekly 30-year fixed rate tracking through May 21, 2026

- NerdWallet Mortgage Rates Database — Real-time rate quotes as of May 23, 2026

- Federal Reserve H.15 Release — Official interest rate data and Fed funds rate policy through May 22, 2026

- CNN Business — Analysis of 9-month high in mortgage rates and economic drivers, May 21, 2026

- JPMorgan Research — U.S. housing market outlook and rate forecasts for 2026

- Morgan Stanley Insights — Mortgage rate and home price forecast through 2026